Hormuz and the Interconnectedness of Commodity Supply Chains

This is a post to apply the humanistic framework set out in my first post to understand the Iran war situation and the causal chain of reactions/effects propagating through energy, agriculture, geopolitics etc. The idea is to identify the causal chain of effects, but not quantify their size/path, as I don’t have enough skill/resources to do that.

I am aware that establishing the chain of effects is one thing but quantifying their exact path in scale and time is another matter entirely.

Mainly summarizing from experts on X:

- Yet Another Commodity Guy

- Rory Johnson

- Stephen Stapczynski

- June Goh

- ABCampbell

- KKGB

- OSINTDefender

- Ole Hansen

- Many, many others (non exhaustive!)

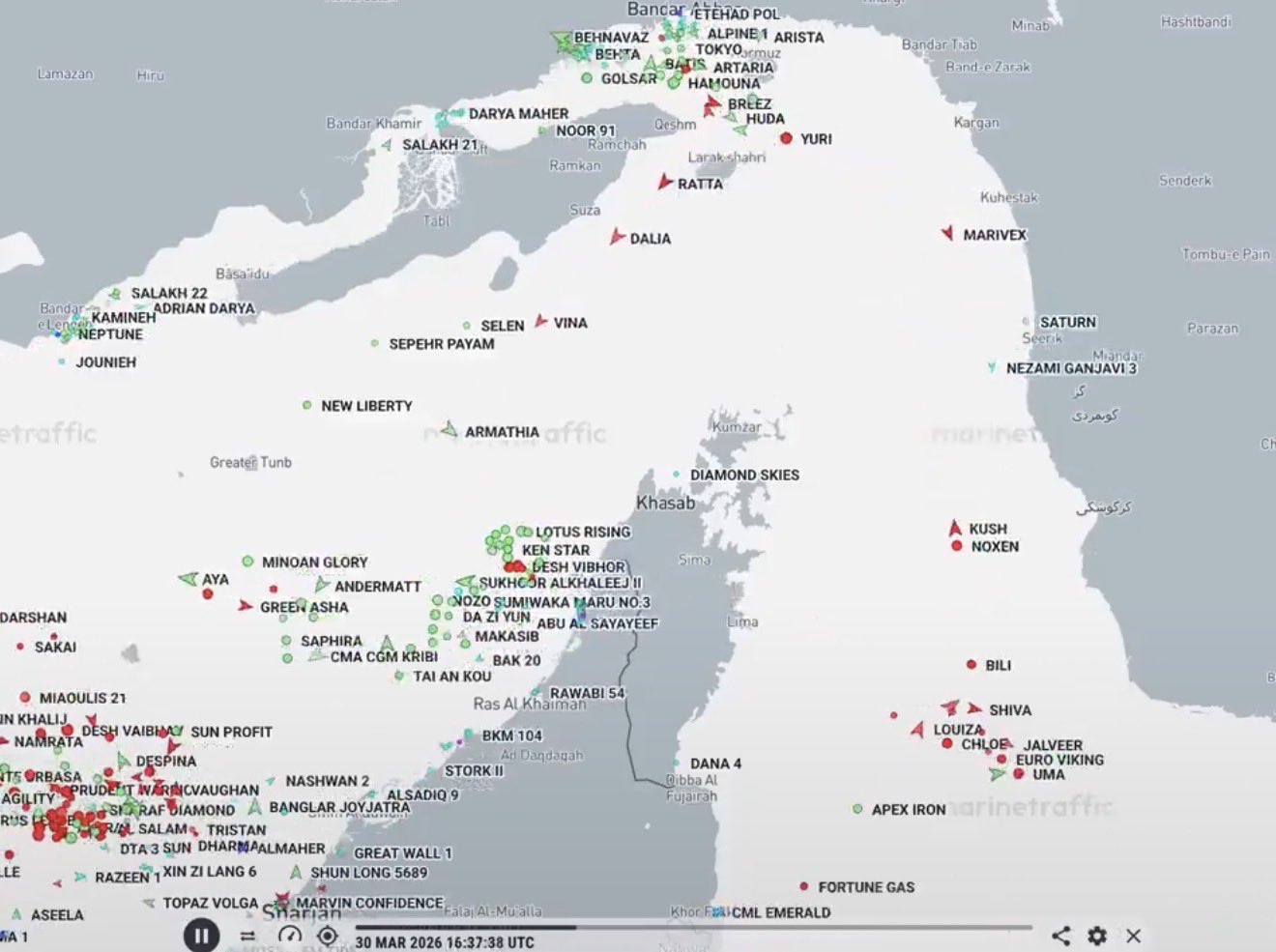

“Monitoring” The Situation

Timeline

After the 12 day war last July, Liberation day tariffs and Venezuela/Maduro capture, Trump decides to go in on Iran with Operation Epic Fury. Is it regime change? Is it denuclearization? Is it a power play against China? Is it a miscalculation? Nobody knows.

The events followed like so: military build up in February, initial strikes and killing of Khameini, the follow up response by Iran on civilian, energy infrastructure, shipping, the IRGC strategy was/is to do asymmetric economic damage by striking unprotected energy infrastructure on GCC countries with drones + the occasional tanker strike to effectively close Hormuz to pressure the instigating US to withdraw, with the most significant being the Ras Laffan strike.

Aside from military response, the response by Administration or by Trump on Truth Social to damage control the energy crisis was things like the EIA SPR RFP barrel loan, 60 day Jones act waiver for domestic damage control, naval escort claims which didn’t happen, suspected Treasury intervention in oil futures, counterproductive easing of sanctions on Iranian/Russian oil.

Then was the 48 hour ultimatum which got TACO’d, the Iranian policy to selectively allow a small amount of certain vessels through with permission, some escalation to power plant/desalination strikes (on Iran by US and on Kuwait by Iran), some crazy trolling by Ghalibaf on X, some OSINT rumours about another military buildup for a land invasion, then the nationwide address by Trump and letter by Pezeshkian, etc. Now the main question for this situation is if another escalation wave will come (and the degree of it) or peace talks will be happening.

Response

The response was an interwoven price shock through supply chains that is propagating the world now with a time lag - mainly in energy/agriculture and downstream industries (e.g chemicals, semiconductors, consumer goods, etc). Which hits developing countries harder as they spend a higher % of income on necessities.

The current equilibrium is the IRGC holding it out and inflicting max pain on the world economy until Trump folds or escalates even further. To me, an amateur, this looks to me like a miscalculation: regime change didn’t do anything, denuclearisation didn’t happen, and Hormuz is now more under Iranian control than pre-war.

I would try to examine, using the humanistic framework in my first post (the idea of situations, actors, actions and reactions) the propagating chain of effects. Again, not quantifying their path, like S/D or barrel counting.

From a markets perspective, the key would be to somehow predict in the military buildup phase that a prolonged war/detente with an energy crisis would unfold, and the faster one realized this, the faster one goes Max Long.

First Order Effects

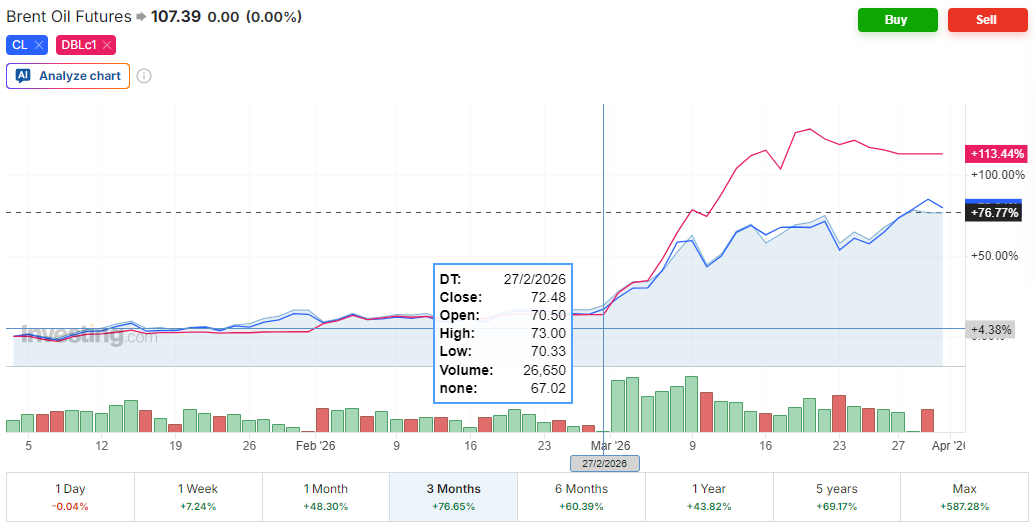

Crude

We can see the market starts pricing in the geopolitical risk premium the moment the Operation happened. Also interesting to see the divergence between the ME oil benchmark and WTI/Brent.

Refined Products

June Goh on X was the first to call the shock in refined products, and also correctly predict, end February, that the shock in refined products would be larger and more disproportionate than in crude. To me, I guess this is because not only are we getting a crude shock from the Hormuz closure, but also a products shock from refinery strikes - both feedstock and capacity.

It is clear that in amongst products, the shock is also uneven, with jet fuel and diesel being more shocked than gasoline. Why? She argues it is the degree of substitution of the product with biofuels and the degree of blending flexibility.

For gasoline, the impact is pump prices. For LPG/naphtha, the impact is petchems and downstream effects like plastics, pharmaceuticals and even semiconductors. For jet fuel aviation cost is the main factor, and for diesel, truck/train freight, agriculture and mining. There is also sulfur exports as a byproduct of refining which then impacts fertilizer/agriculture but is more second order in effect.

The response:

- Demand Control - Rationing measures, work policies - in Southeast Asia, Australia.

- Banning product exports - To preserve domestic economy - China, Russia

- SPR withdrawals - Drawing down inventory - Japan, USA, China

- Substitution effects - E.g gasoline and ethanol blending policy/directives - India, etc.

- Direct and Pass Through Costs/Inflation - Across all parts of the barrel.

- Force Majeure - In Asian petchem plants

LNG

We can see the market starts pricing in the geopolitical risk premium the moment the Operation happened like Crude/Products and also a second surge after the very major Ras Laffan attack, the Force Majeure and some untimely cyclones on Australian LNG, and of course Hormuz closure meaning LNG cargo ships being stuck in the Straits or rerouting to the US.

The main impacts are on Asia and Europe.

Asian LNG to power is impacted as power prices/futures would increase, switching effects occur: short term coal plants running more, so coal demand/price goes up, to replace the gas and oil plants running less, and long term coal/nuke policy, and the power generation cost stack shifts, but the only question is the effect size and timeline, how much impact and when the impact prices in. For nuclear plant policy governments focusing on nuclear plants more is a good thing regardless and is actually a benefit out of this crisis. Pakistan, India, China, Korea, Japan. A power price increase due to LNG dependence also impacts the energy/industry intensive economies of Japan and Korea.

Europe is less dependent on Qatar LNG but the global nature of LNG means maybe cargoes from the US to Europe getting pulled to Asia (more switching effects, but of source rather than of type). Also the post winter storage refill is going on and some countries like Germany and Netherlands have record low storage levels. However from the price chart spot European gas has remained at the price level at the initial war beginning level. So probably spot gas is quite well supplied in Europe for Spring? So I guess the story is in the curve - how warm the upcoming spring/summer will be, and storage level mandates by governments for upcoming winter in November.

Nitrogen/urea fertilizer supply from natural gas affects agriculture/food supply chains, but that is more a second order effect.

Lastly, helium supply which is used in cooling in semiconductor manufacturing, so possibly memory/RAM and processor prices? To my knowledge, semiconductor companies cannot switch or substitute helium out, but also, the current AI boom has already been very bullish for chips and it is not a consumer staple good like food and power/heating is so maybe it is less demand elastic?

Second Order

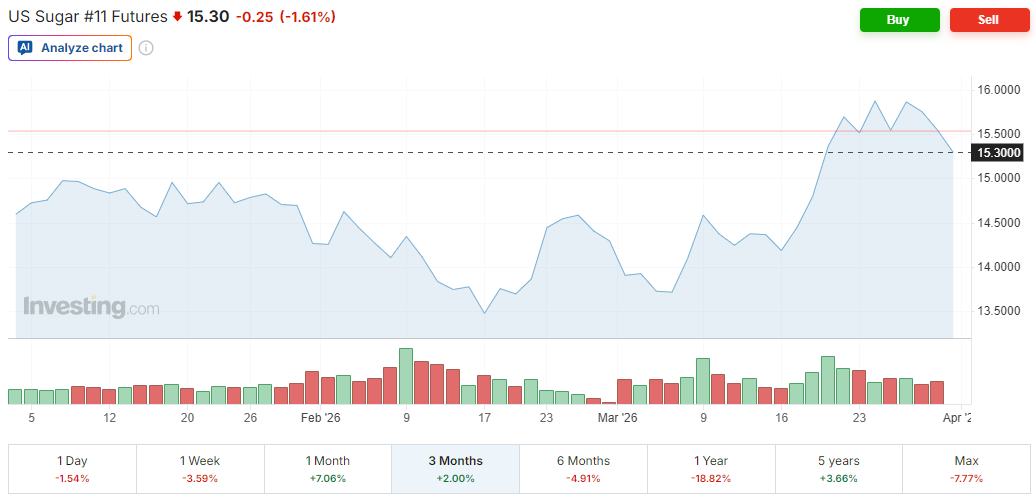

The second order effects on commodities are mostly on agriculture through the fertilizer crisis link and thus lower crop yields in upcoming harvest seasons + the sugarcane to ethanol story as governments mandate for more ethanol blending to alleviate the gasoline shock.

For the former, it is about identifying which crops have greatest sensitivity to the loss of urea and phosphate fertilizer, and to which countries the urea goes to and what mix of crops they grow or export.

Fertilizer

This is mostly from reading Yet Another Commodity Guy’s tweets who is an expert in agricultural commodities amongst other things. To quote his tweet “Hormuz is a giant fertilizer bottleneck”, and the idea is that sugar and ethanol are particularly affected by the Iran situation.

1/2 of world sulfur and 1/3 of world urea goes out through Hormuz as byproducts of refining and natural gas production.

Urea goes to India, SEA, Brazil and urea sensitive crops are sugar, rice, wheat, oil palm. Soybean less as it fixes nitrogen naturally. Phosphate goes to China/India and crop wise goes to corn, soybeans and oilseeds.

There is apparently physical intuition for which crops are sensitive to which type of fertilizer component the most (N, P, K) etc. Leaf intensive crops are more N dependent while seed intensive crops are more P dependent, except soybeans which have lots of leaves but can somehow fix their own nitrogen due to biology.

Agriculture

From another tweet, sugarcane is likely to be the most affected by the urea/nitrogen fertilizer export loss due to losses in Brazil, India and Thailand. What’s worse is China also has implemented a fertilizer export ban in addition and there is a tweet of India’s fertilizer plants that use urea to go round.

Brazil and India dominate sugarcane production/export and USA and Brazil dominate ethanol production from corn and sugar respectively.

Given that governments around the world are increasing ethanol blend % policies into gasoline, this would drive up demand for ethanol exports to alleviate the gasoline crisis.

Of course, I am aware that this is a second order effect and first order effects like the existing situation in the current crop cycle in each country per crop plays a big role, but I do not have information on that.

From a humanitarian, non-markets perspective, developing countries in SEA and India would face rising food costs and the poorer people in these economies suffer most in a reducing in QoL.

However, it seems the supply shock to sugar/ethanol will be in delayed fashion.

Other

Macroeconomy

I don’t know much about this but my guess is there will be some expression in the economies of the more impacted countries like Korea and Japan in their stock and bond markets as inflation sets in due to rising energy costs.

Domestic Politics

It is quite clear that domestic approval in the US voter base for Trump is going down and also spiking gasoline prices in the US won’t do him any favors locally.

There is a tweet on X showing the approval index dropping but another counterargument that this is statistically similar to the last two president’s approval ratings. So I don’t know. What is clear is that this decision has soured international relations both of Trump Administration with NATO and the ME/Gulf states who are not happy about having their very hard to repair energy infrastructure bombed and their main seaborne export channel effectively stopped out.

International Relations

There is some idea in Trump and other Administration members that they expected NATO to support the war effort which did not happen, which is not surprising given the tariff and Greenland situation several months earlier.

I imagine the Gulf States will implement some policies/directives to reduce Hormuz dependence in the next decade by increasing logistics/pipelines etc infrastructure that bypasses Hormuz maybe into the Red Sea.

The Asian countries exposed to this crisis like Japan and Korea also probably are looking efforts to diversify their LNG/oil dependence on Gulf states/Qatar, but all these efforts will play out on a timescale of years to come.

Iran

Nobody has a clue how the post war Hormuz situation will look like. A tolling booth style scenario is in the works, but how would the Gulf States react? Or maybe a long and bloody land invasion with even crazier energy/food shocks and the US controlling Hormuz might occur.

Russia

There was news of Ukrainian weapons aid from the US being diverted to fund the Iranian effort and easing of Russian sanctions to clear the floating storage buffer and increasing Europe energy dependence on Russia looks like the war is very beneficial for Putin, especially if the situations drags on longer and longer.

Summary

So, from what I see on X, and I agree with, the general idea of Trump being so adversarial instead of cooperative eventually will backfire for the US in the long run in terms of trade and economy. Alienation over cooperation is not a good thing. Why he is doing so, I have no idea - obviously he believes in being adversarial, but why is another question. Maybe it’s just the way he operates.

General Learnings

One key idea of the humanistic framework I proposed is that time is a flat circle. Aka certain situations occur involving the same actors and same actions being taken. So we can draw parallels to the last commodity shock due to war, the ongoing Russian-Ukraine war and gas crisis in 2022.

To that, these points follow:

- In a war, escalation follows a ladder, with military targets, followed by critical infrastructure (power plants, water plants, etc).

- Two main conflicts in the 2020s decade have been around sources of energy/agri exporters - so conflict monitoring is very important for energy and agriculture especially if the region/theatre exports commodities, aka ME and Russia.

- Commodity supply shock, due to logistics and transport time on ships/tankers, propagates with a lag, could be weeks or months, depending on distance, and any market might show delayed price impact.

- The impact of one decision or one person can propagate through time in a domino effect and grow in size and scale.

The Humanistic Framework

This exercise is an ex-post application of the humanistic framework to practice - to understand how a situation evolves, action and reaction.

The challenge is to forecast or project any situation and actors reactions ex-ante, early on as possible.

And lastly, another challenge is to quantify these effects (in terms of numbers, dollars, price, quantities in time). To precisely understand the actions and reactions in terms of concrete numbers and details.